Art and the Quality of Money

Since 2018, when I first published this essay in Affidavit, I have had further thoughts on the subject of art and money. The following verson of the essay incorporates these new thoughts.

Money is sometimes easy to quantify. You just add up a column of figures. Sometimes it is not so easy. To calculate the national debt, you would have to mesh advanced mathematics with economics equally advanced. Easy or difficult, the quantification of money is subject to being checked according to agreed-upon standards. Everything changes when we turn from quantities to qualities of money. It’s like turning from math to art—from the verifiable to the imaginary. Think of money laundering, not the process but the idea of it, which follows from the notion that certain money is dirty—not literally but metaphorically. The phrase “mad money” implies that cash can be crazy and when money “burns a hole in your pocket” it is feeling the heat of an acquisitive need. As quantifiable as it is, money is no less qualifiable, and this is nowhere clearer than in the art market.

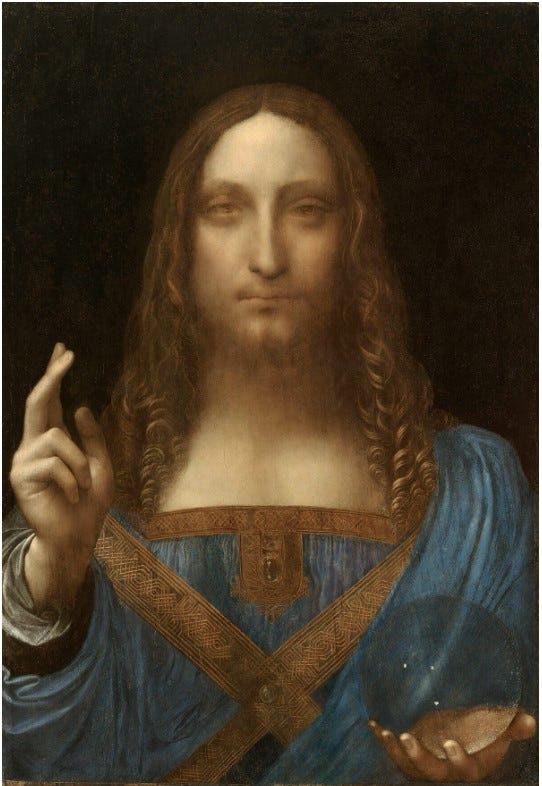

Consider two recent sales, one real and the other make-believe. The first took place in November 2017, when Leonardo da Vinci’s Salvator Mundi went on the block at Christie’s and fetched $450 million. In the second, a young painter’s canvas, on view at a gallery on the Lower East Side of Manhattan, went for $5,000—hardly anything in comparison to the price of the Leonardo. Both sales are art market transactions, and yet this similarity holds only so long as we see money as quantifiable. The moment we acknowledge money’s metaphorical qualities, the purchase of the Leonardo looks less like a transaction in a rational market than the deployment of money as the doppelgänger of a grossly inflated ego. And the $5,000 payment for the work of a young painter looks like a Valentine, for I am stipulating that our imaginary collectors bought this painting with no expectation of future gain. They bought out of love.

Talk of love may sound like a swerve into sentimentality, yet it echoes a hardheaded pamphleteer named J. Jocelyn. Active in early 18th-centry England, he published a polemic favoring free trade policies that ran counter to the conventional wisdom that demanded tariffs and other protectionist devices. Goods, money, and bullion should circulate throughout the world with little or no hindrance, said Jocelyn, prefacing his argument with these remarks:

Value is an Affection of the Mind, and signifies the Liking we have to any Thing, from a Principle of Reason: Love is an Affection like it, and sometimes accompanies it, but that generally proceeds from Passion. There are many Things we Love without Reason, but nothing we Value without [Reason], tho’ very often with a wrong one.

—from “An Essay on Money and Bullion,” 1718

Jocelyn’s syntax may be labyrinthine, yet his main point is clear: economic value is established by “Reason.” Love, by contrast, ignores all rational considerations. At work in the marketplace, “Reason” is the chief faculty of “economic man,” an abstraction that still stalks the sprawling fields of theory. Embryonic in Jocelyn’s tract, adolescent in the writings of Adam Smith and David Ricardo, “economic man” arrives at maturity in John Stuart Mill’s comments on the limits of economics:

It does not treat of the whole of man’s nature as modified by the social state, nor of the whole conduct of man in society. It is concerned with him solely as a being who desires to possess wealth and is capable of judging the comparative efficacy of means for obtaining that end.

—from “On the Definition of Political Economy,” 1836

The capacity for rational judgment is versatile. You could bring it to bear on anything from chess to billiards to the mysterious powder found at the scene of the crime. As rigid as a stick figure, “economic man” uses rationality for just one purpose: to increase profits of a quantifiable kind. Buy low, sell high. Buy a mid-range Picasso for a few million today and sell it for twice the amount five or six years later. That would be impeccably rational, even if you allow for inflation’s effect on the value of the dollar.

But why spend $450 million for a canvas by Leonardo da Vinci that has been heavily restored and is seen as a great painting by almost no one? To flip it for a profit? Not likely. Was this, then, an irrational purchase—the work of “economic man” on a bad day? Or was Salvator Mundi’s buyer in love with it? I suppose Jocelyn’s “Passion” might have driven the bidding to a record level, though it is hard to imagine anyone falling in love with a painting that is not only not great but, let’s face it, mediocre. The most plausible account of the $450-million price tag begins with the likelihood that the buyer was indeed rational, although in a way that economists find difficult to theorize.

At the time of the sale, the new owner was anonymous. After three weeks, the New York Times and other newspapers reported that Salvator Mundi’s purchaser was Bader bin Abdullah bin Mohammed bin Farhan al-Saud, an obscure Saudi prince. Several days later, new evidence suggested that Prince Bader had acted as an agent for his friend, Crown Prince Mohammed bin Salman. Then the Saudi Embassy in Washington announced that Prince Bader acted not for the Crown Prince but for the ministry of culture of Abu Dhabi, in the United Arab Emirates. Much about this transaction is murky and may well remain so. We can be certain, however, that the purchase was meant to establish a record. Previously, the top price for a work of art was the $300 million paid in 2015 for Interchange, 1955, by Willem de Kooning. The new owner of Salvator Mundi has won first place in a competition that has been going on since 1987, when the $39 million paid for Vincent van Gogh’s Vase with Fifteen Sunflowers, 1888, signaled that works of art had become trophies in a newly invigorated game of conspicuous consumption—as Thorsten Veblen called it in The Theory of the Leisure Class.

When that book appeared, in 1899, Henry Clay Frick was jostling J. P. Morgan and other tycoons in the race for old master paintings. Though the tokens in this game have changed—works by the old masters are scarce on current lists of record sales—the game of conspicuous consumption is as lively as ever. Corporations pay immense sums for headquarters buildings in the hope that the public will hail them as landmarks; likewise, those who drive up prices in the art market expect their overpayments to bring them landmark status of a socio-economic kind.

Record prices prompt responses so predictable that it’s rational to play the art trophy game if one feels a need to be the target of abject awe and bitter envy and other dismal emotions. To become that sort of target is not to enjoy a quantifiable benefit. One can put a dollar figure on the profits from a hostile takeover but not on the public reaction to an auction-floor triumph. It’s a matter of quality, not quantity, and even the process of acquiring Salvator Mundi took on a touch of theater at a certain point. Though Christie’s auctioneer was happy to advance the bidding by increments of two to five million dollars, its eventual purchaser took larger steps. The final increment of $30 million is remarkable because a series of smaller ones would have been sufficient. So the jump from $370 million to $400 million (the painting’s price before the addition of a buyer’s premium) was not merely extravagant. It was a gesture with an air of boastfulness, even arrogance, and those qualities now permeate the entire sum—every last dollar—laid out for Salvator Mundi.

Sums that are high but set no records display other qualitative benefits. Say that a buyer pays a blue-chip price in the hope that his purchase will enhance his social status. Or he pays a price with hot-newcomer premium because he wants his purchase to give him access to “a cool lifestyle,” to borrow a bit of patter from the sales pitches of certain art consultants. Money spent for purposes like these takes on a tinge of snobbishness mixed, perhaps, with anxiety about one’s place in the world.

The likelihood that the purchase of a work of art will bring a status boost or increase one’s coolness quotient is not subject to precise measurement. “Economic man” prefers safer bets. Nonetheless, the sort of acquisition we might call snobbish or aspirational has a crucial resemblance to a transaction that produces an easily reckoned profit: it is a means to an end. For better or for worse, most actions are self‑interested. Yet we do some things for their own sakes; moreover, we possess some objects because we find them valuable in themselves. Ancient in origin, the idea that an action or an object can be inherently valuable took on a new salience under pressure from early modern science and technology.

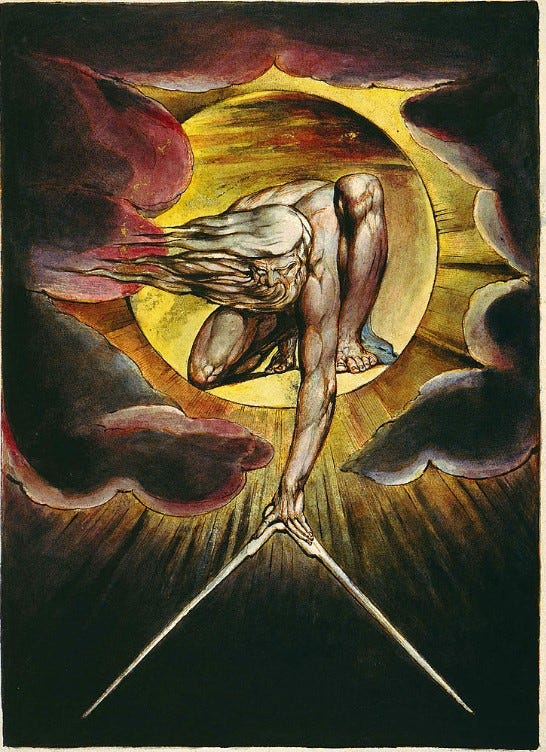

Dazzled by Isaac Newton’s analysis of the physical world, Claude-Adrien Helvétius, the Marquis de Condorcet, and other luminaries of the Enlightenment tried to adapt his theorems to everyday life. Society would run with machine-like efficiency, said Condorcet, if it redesigned itself according to principles derived from a Newtonian analysis of human behavior. Better living through quantification, you might say. Appalled by this mechanistic utopianism, William Blake took Newton as the model for Urizen, the allegorical figure of patriarchal Reason who appears in many of Blake’s poems and prophesies of the 1790s. Bent on reducing the universe to a system of means calibrated to ends, Urizen is “economic man” raised to the scale of myth.

Though he was anything but Blakean in sensibility, Immanuel Kant shared the poet’s horror at the thought of a world comprised only of opportunities for utilitarian calculation. In a world so conceived, even human beings would be treated as means to ends—and this, Kant believed, is the worst sin. If we are to realize our humanity, we must treat others as valuable in themselves. Incessantly rethought by poets and philosophers of the Romantic period, Kant’s concept of the self took a sideways leap in Théophile Gautier’s “Preface” to Mademoiselle de Maupin, a novel published in 1835. At that moment, the inherently valuable person was poised to find a counterpart in the work of art valued for its own sake.

Exasperated by “utilitarian critics” who comb through novels in search of solutions to social and political problems, Gautier insisted in his “Preface” that writers and painters and sculptors have but one proper goal: to create beauty. He did not mean beauty calculated to render our surroundings more pleasant, much less beauty laid on to make moral lessons more palatable, but, rather, beauty absolute and autonomous. From Gautier’s vision of beauty unencumbered by usefulness followed the notion of art for art’s sake and all the ideals of aesthetic purity that proliferated in the Parisian avant-garde of the mid-19th century, in the dreamy dogma of turn-of-the‑century Symbolists, in the formalism of Roger Fry and Clive Bell, and elsewhere. Despite the differences between these doctrines, they all posit an affinity between an inherently valuable work of art and a human being as conceived by Kant. Both artwork and person deserve to be prized for and as themselves, not because of the uses to which they can be put. And the ultimate way to prize a person or a work of art is to fall in love with her or him or it.

To love an artwork is to step out of the world populated by “economic man” and mapped by his narrowly rational reckoning. For it is neither rational nor irrational to love an artwork; it is to respond, imaginatively and empathetically, to a presence comparable to one’s own. In my fictional example, the price of the loved artwork is low, to provide a sharp contrast to the $450 million spent on Salvator Mundi, but it could of course be high. High or low, an expenditure made for love is the metaphorical equivalent of an embrace, and thus it imbues money with Jocelyn’s “Passion.” When money acquires that quality, its significance is no longer solely economic. That is why I said at the outset that we should not see the exchange of money for an artwork one loves as a market transaction. It has its meaning primarily as an act of devotion, albeit secular.

Thanks for this Carter; this is well argued. Yes, it is an act of devotion, of love and praise.

I recall a New Yorker cartoon, depicting a collector showing a friend through his exhibition warehouse. The collector exclaims, " my Braque's are here and over there my Cezanne's ", as he points to crates with those names on them. But, this is humor and perhaps an expression of envy upon real collectors. In my experience, love and admiration is the motivation.

You have made important points about today’s art and its market. These thoughts deserve a wide audience.